Recent data has revealed that inheritance tax (IHT) receipts reached a record level in the 2022/23 tax year.

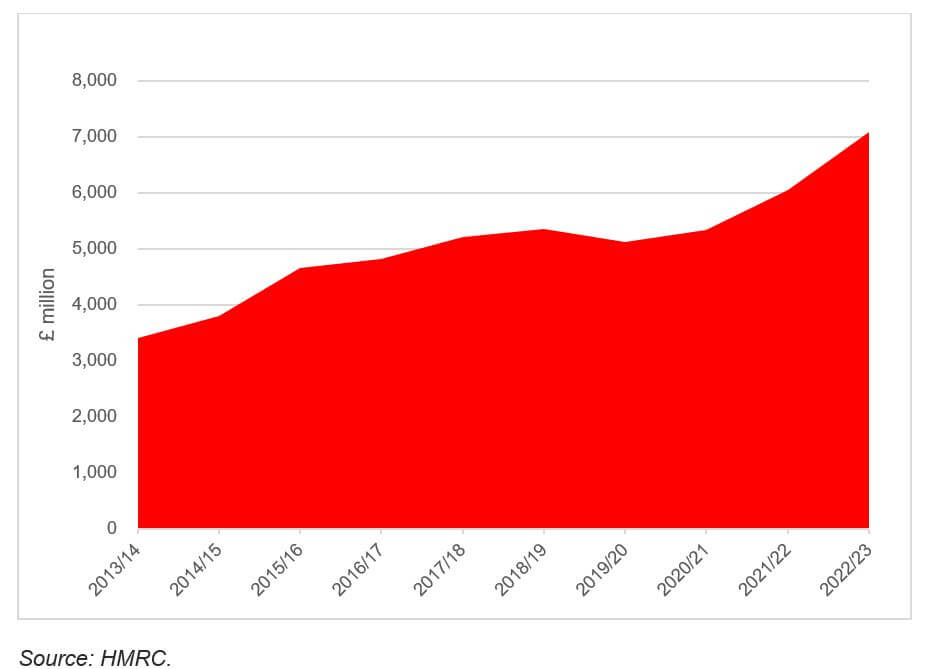

Every month the government publishes data that sets out HMRC’s cash tax receipts in detail. The data issued in late April provided the first set of figures for the sums raised in the 2022/23 tax year. This showed that between 2013/14 and 2022/23:

- Overall HMRC receipts rose by 59.6%;

- Income tax receipts increased by 57.3%; but

- IHT receipts jumped by 108.3%.

For comparison, between April 2013 and March 2023, prices rose by 31.1%, using the CPI as a yardstick.

As the graph shows, the path to the more than doubling of IHT receipts was not smooth. Receipts barely changed between 2017/18 and 2020/21, mainly due to the phased introduction of the residence nil rate band (RNRB) and low inflation. However, in the following two years, the IHT cash entering the Exchequer’s coffers rose by a third. That reflected both the end of the RNRB phasing and the rise in inflation.

Inflation is particularly important for future IHT receipts as both the main nil rate band and the RNRB are frozen at their current levels – £325,000 and £175,000 respectively – until at least April 2028. Such a prolonged freeze at a time of high inflation is a classic example of a stealth tax increase, dragging more estates into the IHT net and raising extra tax from those already caught.

Shortly before the 2022/23 IHT data emerged, the government quietly announced a technical change in its approach to discounted gift trusts, which have long been popular for IHT planning. The unexpected change was the first since 2013 and has reduced the attractiveness of the scheme for potential investors. Fortunately, there remain plenty of other options to mitigate the impact of the tax, from other lifetime trust-based arrangements to the careful structuring of a will.

IHT is a complex tax that requires a holistic, long-term approach to planning. If you would prefer more of your wealth to pass to your chosen beneficiaries rather than to HMRC, the sooner your plans begin, the better.

Tax treatment varies according to individual circumstances and is subject to change.

The Financial Conduct Authority does not regulate tax advice, will writing and some forms of estate planning.

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

The contents of this article are for information purposes only and do not constitute individual advice.